Have you ever been told…

“To buy a home, you must pay at least 20% of the property price as a deposit.”

So what do you do next?

You either:

- Agree with whatever the bank says, or

- Ask questions, and end up even more confused (especially if you’re a first-time home buyer).

And in that confusion, you might make a decision that benefits the bank more than it benefits you.

Yes… the bank.

Because Lenders Mortgage Insurance (LMI) is designed to protect the lender, not you.

Surprised?

Don’t be. While LMI mainly protects the bank, it can also work in your favour, but only if you make a smart and strategic decision.

And for every strategic finance decision, JH Finance Group has your back.

We are always here to rescue you from every confusion related to finance, from a car loan to a home loan; we will guide you throughout the process.

And this blog is doing the same.

So let’s break it down, Lenders Mortgage Insurance (LMI) in simple words for you, so you can buy your home without any extra hassle and save money for your other life plans.

What is Lenders Mortgage Insurance

Lenders Mortgage Insurance (LMI) is an insurance policy that protects the bank, not you, if you can’t repay your home loan.

When you buy a home, banks usually prefer that you pay at least 20% of the property price as a deposit.

Why?

Because when you put in 20% of your own money, the bank feels safer. It means:

- You are financially prepared

- The bank is lending a smaller amount.

- The risk of loss is lower.

For example, Sarah wants to buy a house worth $500,000.

But, for some reason, she is unable to mannage 20% deposit amount and only has a $50,000 (10%) deposit.

So the bank says, “If you don’t have enough savings (less than 20%), Its Okay, we will still lend you the money… but we need insurance to protect ourselves.”

That insurance is called Lenders Mortgage Insurance (LMI).

It helps Sarah buy a home sooner, but it protects the lender, not Sarah.

It means that when your deposit is less than 20%, the bank sees it as a riskier loan.

So they ask you to pay LMI to protect them in case you stop making repayments.

But there is another similar insurance for borrowers called Mortgage Protection Insurance. And people easily get confused here.

(It is a type of insurance policy designed for borrowers. It helps pay off or reduce your home loan if something unexpected happens to you.)

Therefore, let’s first discuss what lenders’ mortgage insurance and mortgage protection insurance are.

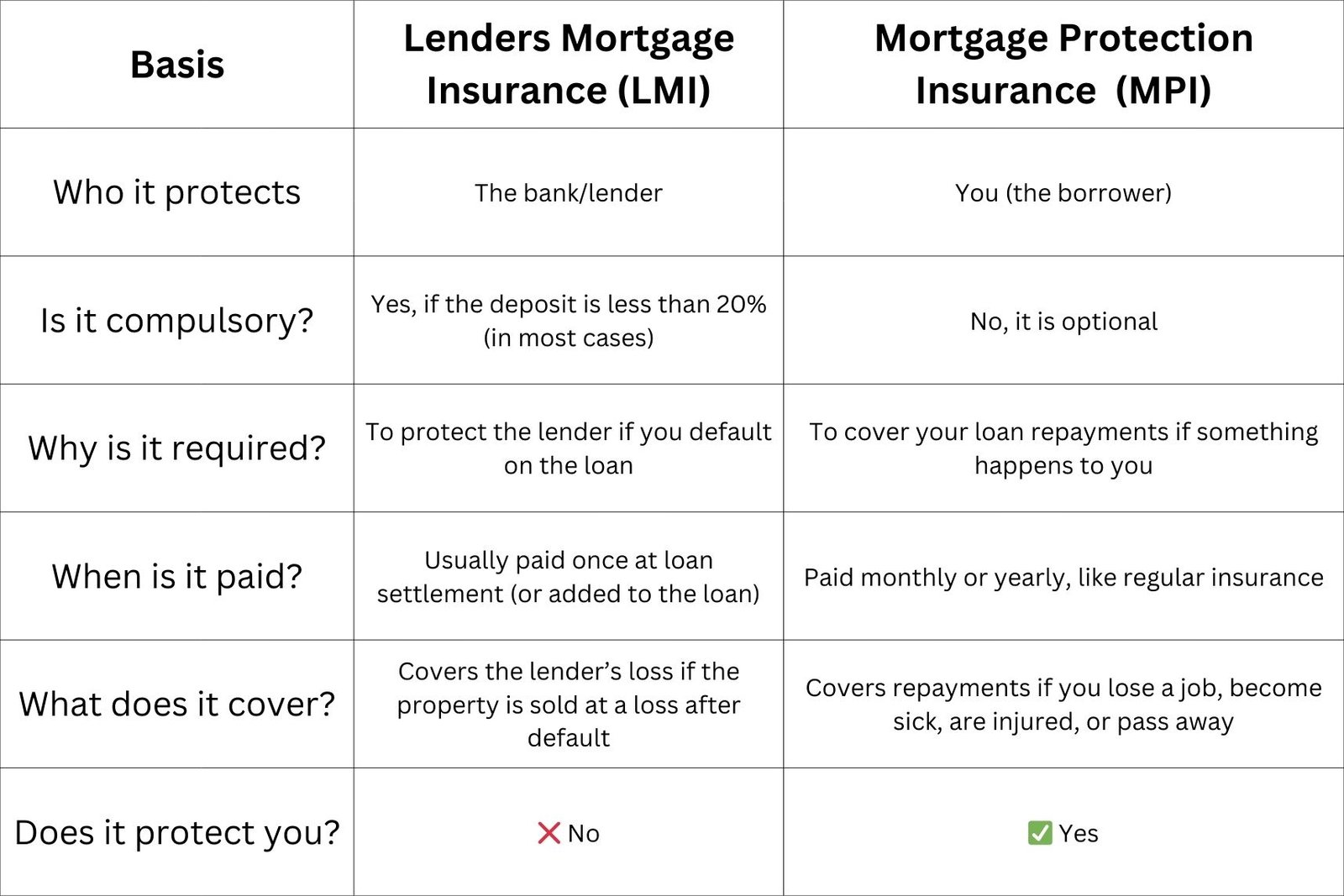

Difference Between LMI and Mortgage Protection Insurance

People easily get confuse in these two Lenders Mortgage Insurance (LMI) and Mortgage Protection Insurance (MPI).

But both insurance has huge differences. One that benefits the bank and also benefits buyers. For a better understanding, read the table given below.

Should You Pay LMI?

The honest answer is: It depends on your situation.

LMI is not good or bad by itself. It’s a financial tool. The real question is:

Does paying LMI help you move forward financially, or is it costing you more in the long run?

Let’s break it down clearly.

If your home loan deposit is less than 20% and has no guarantor, you need to pay LMI.

LMI is typically charged at loan settlement, as a one-off premium either paid upfront, or added to your loan amount (which means you’ll pay interest on it).

Most borrowers choose to add it to the loan to reduce upfront costs.

How Much Deposit Triggers LMI?

- 20%+ deposit → No LMI

- 15% deposit → Small LMI

- 10% deposit → Higher LMI

- 5% deposit → Significant LMI

The exact cost depends on the loan size, deposit percentage, and lender policy.

Pros And Cons Of LMI For Borrowers

Pros of Paying LMI

- Enter the property market sooner – You don’t have to wait years to save a full 20% deposit.

- Buy with a smaller deposit – It allows you to secure a home with as little as 5–15% saved.

- Access better properties sooner – You may be able to purchase a higher-value or better-located property earlier.

- Potential capital growth benefits – If property prices rise while you’re waiting to save, entering early could outweigh the LMI cost.

Flexible payment option – LMI can usually be added to your loan instead of paid upfront.

Cons of Paying LMI

- It’s an extra cost – LMI is typically calculated at up to around 5% of the loan amount, which can mean thousands of dollars.

- You pay interest on it (if added to the loan) – Capitalising LMI increases your loan balance and total interest over time.

- No direct benefit to you – LMI protects the lender, not the borrower.

- Higher overall repayments – A larger loan amount means higher monthly mortgage repayments.

Could be avoided with more savings – Waiting to build a 20% deposit may eliminate or significantly reduce LMI.

Buy your own home.

Find the home you love without overpaying. We secure Australia’s lowest home loan rates so you can save thousands.

What Happens When We Are Unable To Pay LMI?

Lenders Mortgage Insurance (LMI) is usually required when you borrow more than 80% of a property’s value.

But what happens if you can’t afford to pay it?

Here’s how it typically works.

1. If You Can’t Pay LMI Upfront

In most cases, you don’t actually need to pay LMI in cash at settlement. Lenders usually give you the option to:

- Add (capitalise) the LMI premium to your loan

- Pay it upfront as a one-off amount.

If you can’t afford to pay it upfront, the lender will typically add it to your loan balance.

However, this increases your total loan amount and the interest you pay over time.

2. If You Can’t Qualify Because of LMI Costs

Sometimes the issue isn’t paying it upfront, it’s that adding LMI pushes your loan too high.

This can happen if your borrowing capacity is already at its limit or your loan-to-value ratio (LVR) becomes too high after adding LMI.

In this case, your loan may be declined unless you:

- Increase your deposit

- Purchase a lower-priced property.

- Use a guarantor

- Apply for a government first-home guarantee scheme.

3. If You Default on Your Loan Later

It’s important to understand that LMI protects the lender, not you.

If you default on your mortgage and the property is sold for less than the outstanding loan:

- The lender claims the shortfall from the insurer

- The insurer may then pursue you to recover the debt

So even though LMI is paid, you are still responsible for the debt.

5 Tips: How To Play It Safe Side?

1. Aim for 20% deposit:

The safest way to avoid LMI is to keep your loan-to-value ratio (LVR) at 80% or below.

Borrowing more than 80% of the property value usually triggers LMI, which can cost thousands.

- Delay purchase slightly

- Boost savings

- Negotiate purchase price

- Consider smaller/entry-level properties.

Sometimes waiting 6–12 months can save you $15,000–$30,000.

2. Check If You Qualify for an LMI Waiver:

Some lenders offer LMI waivers for certain professions (e.g., medical, legal, and accounting professionals).

- Ask your broker or lender specifically about professional LMI waivers.

- Don’t assume you must pay it; policies vary between banks.

Many buyers never ask and miss out.

3. Compare Lenders, Not Just Interest Rates:

Different lenders calculate LMI differently. The premium can vary significantly. In two scenarios:

- Compare total loan cost (including LMI), not just interest rate

- Request a written breakdown of LMI costs before applying

The cheapest rate doesn’t always mean the cheapest loan.

4. Understand Capitalising LMI:

You can add LMI to your loan, but that means paying interest on it for years.

Confirm with your lender first that:

- LMI will be paid upfront, or

- LMI will be added to the loan

Compare the total repayment difference before making the final decision.

5. Run the “Wait vs. Pay” Calculation:

Sometimes paying LMI is smarter than waiting to save 20%, especially in a rising market. To Play-it-safe compare:

- Cost of LMI

- Potential property price growth if you wait

- Rent paid while saving.

LMI isn’t always bad, but it should be a strategic decision, not a surprise.

How Does JH Finance Group Help You With LMI?

JH Finance Group helps first-home buyers, property investors, and small business owners understand Lenders Mortgage Insurance before they borrow.

We explain when LMI applies, how much it may cost, and whether it can be reduced or avoided.

Our team compares lenders to find competitive loan options, not just the lowest rate.

We structure your loan strategically to support your long-term financial goals.

With clear advice and no surprises, we help you secure the right loan with confidence.

Bottom Line

Lenders Mortgage Insurance (LMI) protects the lender, not you.

When your deposit is less than 20%. While it’s an extra cost, it can also help you enter the property market sooner if used strategically.

The key is understanding when it applies, how much it costs, and whether paying it makes financial sense for your situation.

At JH Finance Group, we help first-home buyers, investors, and business owners understand LMI and secure the right loan with clarity and confidence.

Connect with our financial broker to get Smart advice and a clear strategy.